Most of the world knows by now of the death of North Korea's dictator, Kim Jong Il. You may also know it took more than 48 hours before the information was publicly announced to the world and the announcement came from the North Koreans themselves and not from any western intelligence services.

The New York Times recently ran an article claiming this is a failure of western intelligence services:

For South Korean and American intelligence services to have failed to pick up any clues to this momentous development — panicked phone calls between government officials, say, or soldiers massing around Mr. Kim’s train — attests to the secretive nature of North Korea, a country not only at odds with most of the world but also sealed off from it in a way that defies spies or satellites.

My question to the New York Times and everyone else is how do you know we didn't know about it? IF our intelligence agencies had picked up the information and then broadcast this news to the world do you think this would have been a good use of that intelligence gathering method? News and information coming out of North Korea is challenging at best so IF our spooks had a channel to this sort of high level information why should we let the North Koreans know we have the information ourselves?

During the Clinton administration it was leaked that our CIA was spying on the Japanese during trade negotiations. Talk about short sighted. If you are successfully gathering information why go public with your success? From the LA Times:

Among the successes, sources say, is strong intelligence information the CIA provided on the Japanese during this spring's heated auto trade negotiations between the Clinton Administration and Japan. "We've done really well with the Japanese," one source said.

Now of course it is entirely possible our spooks did not find out about Kim Jong Il's death until the public release. I hope not but it is entirely possible. If so there is hope on the horizon. In 2008 Orascom was granted a monopoly license to provide cell phone service in North Korea.

Orascom Telecom Holding was awarded a Greenfield license to establish and operate a WCDMA (3G) network in DPRK in January 2008. koryolink was launched in December 15th 2008 as a joint venture between OTH (75%) and Korea Posts and Telecomm Corp. (KPTC) (25%). koryolink has deployed its 3G network to initially cover the capital Pyongyang - which has a population of more than 2 million - with an ambitious plan, already under implementation, to extend coverage to the entire country. OTH has over 431 thousand subscribers and 100% market share as of December 2010.

All it would take is a few well placed bits of hardware and software installed onto that network to provide a flood of data for our intelligence services to chew through. Furthermore cell phone transmissions can be remotely detected and analyzed if a physical connection to the network cannot be obtained. As the North Koreans discover the convenience of cell phones the challenges of intelligence gathering will lessen.

How much better can it all get? http://t.co/yyRRYdfv ---- Looking at whether all the good/bad news is out RT @jennyandteets: Guys, know who likes to hear about your fantasy football team? Your fantasy girlfriend #yourekillingme -- I have enough problems with the real world, I don't need to stress about my fantasy life as well.

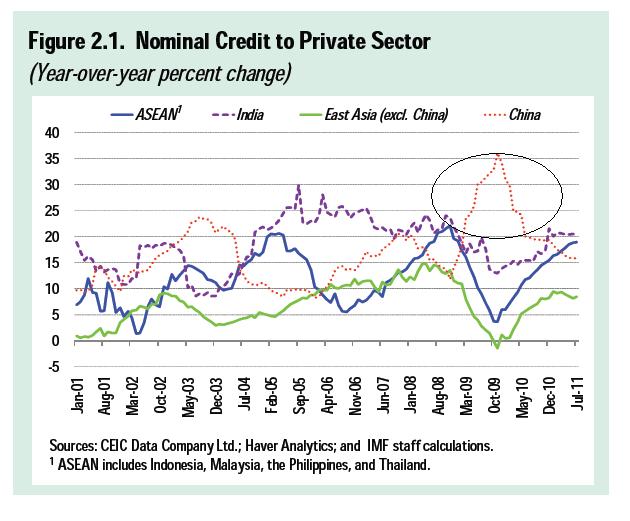

Earlier this month I highlighted the continued deceleration in Chinese lending growth from it's peak in late 2009. Just how massive their credit growth was unknown to me until this recent post and chart by Global Macro Monitor

The growth in lending right after the 2008/09 credit crisis is truly spectacular, even compared to other high growth Asian economies. I'll snicker even more when I hear talking heads gush about how the Chinese mandarins were able to 'navigate' their way through the economic crisis and their ability to manage such a large economy.

Bunk.

They just called up the bankers and said LEND.

The bankers asked, "How much?"

It was not some Chinese mastery of the economic cycle or superior technocratic skill; it was simply an ability to throw lots of money at the problem. Unfortunately for China the bill is now coming due.

Here's an update on inflation expectations as expressed by the bond market. As the nominal 10 year yield continues to drop it has pushed the TIPS real yield to nearly zero. Some investors may grouse at the option of buying a security that guarantees a zero real return for the next 10 years and I agree with their sentiments.

As to why this situation exists I would suggest it is a result of the Fed's desire to reflate the economy by numerous unconventional means (zero short rates, all the various flavors of QE)

The spread between nominal and real yields has remains remarkably stable near the 2% mark with some noise on either side. If we have another financial crisis, this time in Europe, I wonder if we'll see another drop in the implied breakeven rate....

Some reading material for you from my twitter stream:

http://t.co/vXWLZxuV - Italy near tipping point of increased margin requirements. I'm not the only one talking about this RT @zerohedge: Hugh Hendry says he has made bets that will deliver a 40-to-1 return if the ECB cuts rates below 1% next year http://t.co/PAv4msUK RT @edwardnh: The fact Greece's exit from euro has been discussed openly is seismic shift http://t.co/QVaWF7si I'll get bullish when this stops going up. http://t.co/6vmUhc60 97% of family businesses don't make it past the 3rd generation http://t.co/MZAwrwRK RT @FGoria: MT @M_McDonough: Italian CDS implying, country may be at risk of losing its investment grade status: http://t.co/mIVWCwkk RT @mbusigin: Note that we did work on this in August, which gave us a different (bullish) signal: http://t.co/ivxLrhzB RT @mbusigin: The few times realised volatility has eclipsed implied volatility, it presaged large declines: http://t.co/zTRw4ZDE RT @edwardnh: Greece gets ultimatum: accept austerity plan or forgo extra bailout cash | Business | The Guardian http://t.co/DZSOBkDY -- Greece later backed down. RT @edwardnh: France and Germany to withhold aid, Greece to be ejected http://t.co/WtNwsF6M#in $$ Greek referendum provides political cover http://t.co/MFDzDUCk RT @PragCapitalist: THE GREEK REFERENDUM AND THE ROLE OF DEMOCRACY: I set off a bit of a firestorm on Twitter this afternoon when I ... http://t.co/O8GZFHvQ New international bond etf's for Germany, Canada, and Australia $aud $cad $bund http://t.co/OemicVIk Balestra Capitals Matthew Lucket Talks Gold, Deleveraging Story, and China Credit Problem http://t.co/9vGl387V@historysquared

It has been over a year since I last highlighted the slow decline in official lending statistics out of China. Since then not much has happened regarding the direction of Chinese lending growth; a slow decline continues.

I point you to Steve Keen's debtwatch for why the rate of growth in lending is important.

The rate of lending growth peaked in October 2009 and has been declining ever since. Compare this to the Chinese equity markets and you'll see how Chinese stocks haven't gone anywhere since October '09 either.

Unofficial lending is naturally harder to track but there are anecdotal signs of stress in this sector as well. http://historysquared.com/ and http://www.alsosprachanalyst.com/ are two good sites to follow the 'underground' lending market.

I find this episode of Hendry publicity a little different as he discusses his trading style and aspriations of what he wishes he could be as an investor. If you cannot watch the entire series I suggest you at least watch episodes 4 and 5. Realizing you don't know the future and how having too much knowledge can be detrimental really struck home with me. If you study a company too much you can fall in love with the security, even as it goes down, down, down, and .... down. Someday I may gather up enough courage to relate my failures in this category.

Even before the Greek referendum drama of the last 24 hours the bond market was not impressed with the latest Euro crisis 'solution'.

With Portugal, Ireland and Greece all tipping over the edge the next domino to watch is Italy.

Last week's news of a 50% 'voluntary' haircut for some Greek debt vaulted world equity and currency markets higher in a massive relief and short covering rally. Mr. Bond market was not so impressed.

While both the absolute and relative yield of Italy's 10 year bond did fall a bit late last week on the news of the news of a new solution to the Greek debt situation announced Thursday morning by Friday afternoon Italian yields were creeping upwards again.

The news of a Greek referendum on the latest round of negotiations shocked the markets and drove almost every risk asset downward with only the dollar and US Treasuries rallying. Italian yields are not looking good from a technical perspective and if they break 7% it could be the final domino to fall before the real euro crisis starts. I'll be watching these metrics closely.

Some reading material for you from my twitter stream:

RT @edwardnh: Why the latest eurozone bail-out is destined to fail within weeks - Telegraph http://t.co/sgj8HQcn RT @credittrader: GReader: The Global Moral Hazard Dawns: Merkel Says "It Must Be Prevented That Others Come Seeking A Haircut" As... http://t.co/Tjd22kbQ RT @theanalyst_hk: $$ Jim Chanos: Not Impressed By The Europeans, And Still Shorting #Chinahttp://t.co/OvdXeWIr#economy#europe RT @JackHBarnes: Chart of the Day: North Dakota Annual Oil Production: http://t.co/lUWOqWst -- need to do more research myself on shale oil Transfer payments over time in US http://t.co/sxiw6sF8 RT @zerohedge: And Now, For Some Semblance Of Sanity, Here Is One Hour Of Hugh Hendry http://t.co/5A5Jwgxu -- separate post on this soon(tm) CITI: Failure To Trigger Greek CDS Could Cause The Whole Euro Bailout To Fall Apart http://t.co/TLDjUF7L -- be careful what you wish for Meanwhile in China a swan finally takes flight... http://t.co/Z8w40PKd -- Condo prices are falling hard. RT @AlephBlog: Fannie Squeezing Banks Makes 4% Mortgage a Mirage, Hinders Housing Rebound http://t.co/BKikceRX Higher lending standards fight lower rates RT @AlephBlog: Money managers and commodities, the case against http://t.co/ynsn1qT3 Graph shows $$ managers drove commodity prices http://t.co/eNKE3nFA RT @andrewyorks: *EU LEADERS CALL FOR BANKS TO HAVE 9% CORE CAPITAL LEVEL ok move that dial on the upper left to 9 http://t.co/WHLMk6Dm -- should be interesting when taking haircuts on Greek debt. Skyscraper taller than any in London or Tokyo opens in Chinese village of 2000. http://t.co/IvHoRw4j#thiswillnotendwell Underground bank lending in China - NPR - http://t.co/677IPKYK RT @historysquared: $$ The cash commodity trading firms that account for 1 trillion in annual revenue 50% of all transactions http://t.co/TqTvhHM1 RT @ftasia: Iron ore plummets to 15-month low: As Chinese steel mills cut production, the price of iron ore dropped 7.2 per ... http://t.co/RVfC48zy Blackberry outage made roads safer. http://t.co/agSNxNGX

RT @FactSet: What do yield curves tell us about the outlook for the world #economy? We take a look: http://t.co/r4ucgUfl -- Inverted Yield Curves are bad....

RT @NicTrades: FT: French banks curbing credit lines for commodities trading http://t.co/62sZhIkB -- What do you think will happen to all the base metals when Greece goes POP! ??

#copper getting crushed today. Will it completely break down or bounce off the bottom again? http://t.co/2h0LKT31 -- looks like it bounced.

Ray Dalio of Bridgewater Associates has recently appeared on the Charlie Rose show as well as written a piece for the Financial Times. I think he does a good job of describing how we got here (continually borrowing money to improve our standard of living) and the tenuous situation we find ourselves in (Greece, falling home prices, etc.)

We are in the midst of a deleveraging, we are nearly out of ammunition and we are at each other’s throats. Being in a deleveraging and nearly out of ammunition is a very difficult position to be in. But, being at each other’s throats is our biggest problem.

Our character and our political and social systems are now being tested in ways that have typically been tested in past deleveragings. In deleveragings bad economic conditions typically lead to emotional reactions, social and political fragmentation, poor decision-making and increased conflict. When this occurs in democracies, the checks and balance system, which is intended to yield the best decisions for the whole, can stand in the way of thoughtful leadership and lead to ineffective “mob” rule. This dynamic can lead to a self-reinforcing downward spiral.

The video goes into a little more detail of his philosophy of knowing what you don't know and being willing to have your ideas and conclusions challenged throughout the corporate structure. I suggest you read both the article and watch the interview.

I don't usually comment on the price of the equity markets but considering what I'm seeing I thought I'd bend one of my self imposed guidelines. Remember you are hearing this from someone who does not see any positive forces influencing the market right now.

The markets have been pretty much stuck in a rut since early August and seems to be driven by the constant stream of contradictory rumors coming out of Europe. Will they save Greece? (no, they can't) Will the European banks be nationalized? (no idea, but I'm not hanging out to find out) Meanwhile China's negative real rate maneuver and excessive credit creation is coming back to haunt them. And America is slowing down.

Stuck in a rut for the last two months.

Here are some of the indicators I look at to assess financial market risk and as you can see all of them are going the wrong way.

Notice how the TED (Treasury - Eurodollar spread, an indicator of banking stress) peaked and started healing before the market bottomed in early July 2010; showing a positive divergence.

The spread for emerging market bonds also shot up before the correction in 2010 and also showed a similar positive divergence. Right now spreads continue to widen.

My own proprietary indicators are not showing any sort of improvement either, again the opposite of 2010.

Note how in 2010 risk stopped going up.

Compare to 2011 where the RiskMeter keeps going up.

Do I think the market is going to crash? I can't answer that question. If the European situation looks like it can be truly resolved we could get a serious rally. I'm waiting to see what my fundamental indicators of market health tell me before I get back into the stock market.

Right now they are saying wait.

Remember, no matter what happens there's someone out there who'll be trying to convince you to buy stocks right now.

Humble Student of the Market - Germany engaging in expensive can kicking. We may get a bounce but it does not fix the fact Greece has too much debt. Who owns it is immaterial.

The recent drop in long term yields is impressive and historic. While the 30 year treasury yield has backed up a bit it is still very low, currently in the range seen during the depth of the financial crisis of 2008.

I'm not trying to convince you of whether it can go lower in this post even though I currently own long term treasuries. I'm considering selling of some of my position and this blog post is part of me thinking aloud about the situation.

What is interesting about this current phase of declining interest rates is how the 10 year has broken new lows while the 30 year, while low, is not in record territory yet. (Note the 30 year was not issued for part of the 2000's. You'll see gaps in the data during that period)

30 and 10 year yields

Looking at the difference between 30 and 10 year yields provides a very different picture.

30 year less 10 year yield

While the spread has declined recently we are still in rare territory when the difference between the 30 and 10 is greater than 1%. What this all means I honestly don't know yet but I thought I'd share with you yet another example of how our unique our current situation is.

The author owns long term treasuries and is considering paring back his position.

A little more than six months ago I laid out a bearish case for the red metal, also known as Dr. Copper by those in the markets for its ability to predict future economic change. With the recent thrashing copper and many other risk assets have taken I thought revisiting the topic would be a good idea.

While China is a large factor in all base metals prices let's start with the Old World and the seemingly mundane issue of actually counting how much copper inventory is on hand. While this would appear to be as simple as looking up the LME (London Metal Exchange) and COMEX (US futures) inventory numbers it really isn't. The BBC ran a three part series on rising commodity prices in late May and spent nearly a third of the program on copper.

BBC Radio - Bubble Trouble - Part 1 - May 28,2011 BBC Radio - Bubble Trouble - Part 2 and 3 Ft.com blog highlighting the inventory issue

In part 2 around the seven minute mark the presenter takes a tour of a well known base metals warehouse in which the warehouse representative reveals only about 40% of the copper in the warehouse is registered as LME inventory. When I heard the words I had to replay it several times to ensure I understood that correctly; my brain almost rebelled at the concept of anyone just coming out and publicly stating such a figure. Now I'm not suggesting the LME reported amount is under counting European stocks by 40%, just that this one warehouse has a lot more copper inside its walls that is reported to LME. Please listen to at least part 2 of the radio series to get the full details. If it can happen in one warehouse in Rotterdam what is preventing it from happening elsewhere in the world?

So why is the copper 'hiding'? Some of it is because costs are cheaper to store it in a non registered warehouse versus an official LME warehouse. Another factor may be what is suspected to be going on in China. FT Alphaville has discussed import/export trading firms there are using copper as a credit funding vehicle because other more official forms of credit are drying up.

Here’s the gist of it.In the first instance, our source says, the strategy is not exclusive to copper markets but goes on across most commodity markets.

The banks call it “inventory financing”. And of course, we should stress, it is completely legal. The practice mainly involves pledging an asset in return for an exchange warrant or cash.

According to our source, traders can deposit copper in an exchange warehouse in order to receive a warrant which can then be used to gain financing, usually via a broker, and less a 15 or 20 per cent haircut needed to cover futures margin deposits (sometimes called margin or warrant financing).

Read the whole article to get the full weight of what they are doing. This copper-as-financing would help explain why copper continues to be imported even though for most of 2011 it has been cheaper on the domestic Shanghai exchange. For the credit focused copper trader the money created by the transaction has greater value than the actual copper, it is just a funding mechanism.

While the discount has been steadily falling one must understand China is a net importer of Copper; so why has it been cheaper to buy copper inside China?

Izabella Kaminska followed up a few weeks later with more details on the same copper-as-collateral trade

More worryingly however is that the primary use of copper in bonded warehouse appears to be as a financing mechanism to provide cheap working capital for various types of business often unrelated to the metallic industry.

Having just come back from China my impression is that more and more people are beginning to understand that a lot of copper that has been imported has not gone into furnaces, that it is held by both foreign and Chinese financial institutions and others and I do think that even at the top level in government there is now starting to be a concern of the impact of this speculation on China's economy. Because it is not just copper - it goes much deeper than that. With money which has been so freely available in recent years, and with negative deposit rates, any company or individual is very reluctant to hold funds on deposit. So they are looking for other means of investment and it goes into commodity markets generally - the stock market, it goes into manufacturing investment and so on so forth. Whether government does anything to stop this game going on I've no idea, but there is at least a realisation at a pretty senior level that these developments are ongoing.

Mr. Hunt also brings up the insidious problem of negative real interest rates in a growing economy. Empty cities such as Ordos are an example of what happens when people respond to the obvious distortion of losing money when you put it in a bank account.

The world No.1 copper producer, Chile's state-ownedCodelco, sounded a warning shot at the CESCO copper industrygathering in Santiago on Monday, saying copper stocks in China were abnormally high and needed to be watched carefully.

Figures are tossed about regarding how much inventory has been tied up in these financing deals but one never really knows how much until the real washout hits and people are forced to dump their positions.

That being said, some analysts are putting out huge numbers as to the extent of hidden inventory, again from ft.com blog

The ICSG data shows an increase in Chinese demand of 99% for the four years between 2005 and 2009 when Chinese GDP probably rose by about a third. Obviously, there cannot possibly have been such a massive rise in copper’s intensity of use in China. You can look through all the intensity of use curves for every commodity for every economy in history and you will never find a doubling in consumption against a one third increase in GDP over so short a period of time.

The numbers are large, around 4 million tonnes since the end of 2006. This dates from when global fabricators and others started to understand that a new paradigm in the copper market had begun. It was the involvement of the financial community by buying copper directly from producers and others and warehousing the metal outside the reporting system.

High inventories in bonded warehouses point to the possibility of destocking, which could hit copper prices on the London Metal Exchange (LME). As of this week, we estimate that total copper stocks in bonded warehouses in Shanghai (usually 80% of the national total) have hit 650 thousand tonnes (kt) – equivalent to roughly four weeks of China's domestic use, a record-high level (Chart 2). This is significantly higher than 550kt in late February and the 200kt average over the past three years.

ETFs have been a useful tool to allow banks to move risk off balance sheet. When a bank takes on risk through lending to or financing a big commodity player, say for an acquisition, there is a need to hedge potentially huge commodity exposure — so as sell to lock in the commodity price, and you couldn’t sell that volume easily into the terminal market; although you could transfer a large amount of exposure to investors through an ETF more easily. The only way this used to be done is by the bank taking proprietary risk, but they now have other risk issues and aren’t prepared to carry that sort of exposure.

Using ETFs becomes a mutuality of interest, with everyone moving to launch products to investors – retail and institutional – so that they can carry the risk instead. It’s all about de-risking your book. And you saw it in the dot com bust when investment banks pushed dotcoms, but offloaded the risk to investors. When the NASDAQ crashed the investors carried the bulk of the exposure.It all has similarities to the Abacus CDO. If you want to short the market you have to create the demand, like Paulson did. If you are an institutional advisor you can do that by hyping the commodity.

The actual import numbers going into China for both refined and scrap do not mesh well with the meme of voracious demand. On a year over year basis both are falling.

Furthermore the reported inventory numbers have been wandering around the 600k number for a while. Ironically the last time year over year inventory numbers dipped into negative territory for a while was 2008.

I'm not the only one who is not a copper bull. The Reformed Broker sums it nicely while debating a copper bull:

I will admit some of my thesis is based upon information that is not reported as cut and dried numbers that can easily be looked up on a computer screen but what I do find does not add up to the template of China hoovering up all known copper deposits in the universe:

Copper is cheaper in Shanghai than in London

Copper imports of all kinds are dropping

Public reports of a LOT of hidden copper stocks, in the Old Word as well as China and confirmed by Chileans

I could go on but you need to put in some work as well. Read over the links below. I saved a few bombshells for your discovery...