I've yammered on about this for a long long time. Highlighting empty cities to nowhere, excessive debt buildup, etc. Obviously the Chinese government's ability to extend this bubble is greater than my FinTwit credibility.

Are we hitting another decision point? Will the next US recession finally detonate the bubble? Honestly I don't know, but now ever Peter Zeihan is commenting on this.

The more China blows the debt bubble the larger the explosion when it pops and right now they are working on exceeding the Japanese bubble from decades ago.

A recent tweet by Kevin Smith of Crescat Capital (someone I've had the pleasure of meeting in person)reminded me of just how far we've come since 2008 and the Great Recession.

By how far we've come I'm not meaning in a positive sense. If you look at the selected ratios of debt to GDP for Canada, China, and Australia they've each grown tremendously since 2008/09. While this has helped goose growth in each of their respective economies (and spilled out into the greater world as well) it does not bode well for the future. The thing about debt is it need to be paid off. Somehow, someway (by default, payment or inflation) the ratios will drop when they reach such lofty heights.

Crescat capital annotated the above chart rather nicely showing you the negative events which coincided with either a rapid rise in debt to GDP (like Thailand) OR a high ratio overall (Japan, USA, Spain) Their implication is Canada, China, and Australia are heading toward a likely credit crises and I'm inclined to agree with them.

These are not the only shimmering spheres on the horizon however. Look below and you can see all three of the Scandinavian countries are above US levels before our little economic problem in 2008.

The challenge with calling the tops in a bubble is you are battling central bankers and their willingness to keep the debt flowing. Who wants to say no when the money is flowing? Even central bankers can exhibit human tendencies on occasion, they don't want to be derided for being the Grinch that stole Christmas... As such it's very hard to know when they will finally start to restrict the lending and tighten liquidity. While the US is not at the top of this rarified list it is entirely possible our current series of recent (and future?) rate hikes will be enough to tip one of these countries over the edge which could then get the dominos falling. When is unknown, but that it will happen appears quite likely.

Looks like the Chinese credit impulse may have turned negative recently. As the data presented above is nearly 6 months old this is very interesting. While it ripple through to the US markets? We shall see shortly.

Never bet against The Chanos

That may sound like an odd commandment, but it's a good one. I speak of Jim Chanos, the well known short seller. Speaking highly of a member of such a profession may raise the hackles of some individuals, as well as governments, but I have been following his public pronouncements for quite a while and he may be early, but very rarely wrong. Post the great recession of 2008-2009 he was one of the first to warn about the construction & credit bubbles percolating in China; and while ridiculed for it his warnings have played out.

I even have a google alert on "Jim Chanos" (along with quite a few others) so as to catch everything he talks about. Recently I got a hit on a great 90+ minute podcast he did with FT Alphaville.

It's been a while since I've mentioned Hugh Hendry but he's popped back up on YouTube recently. After his positively raucous returns in the depth of the crisis he had a long period of very underwhelming returns and from his manner in this broadcast I'd guess a tough few years.

As always I find him entertaining to watch. He provides some of the reasons for his reversal of opinion on China as well. Regardless whether you agree with him or not I suggest you listen.

He so kindly provided a video link showing the full scale of the project. While some may claim there is progress and construction still going on, please compare the level of activity to the massive size of the project.

Here's a Google Maps screenshot of the place. Just look at all those skyscrapers that need to be filled.

So what happens when all those skyscrapers go up, no one fills them, and the 'need' for more slows down? Iron ore prices fall back into the earth

I have discussed copper before and something recently caught my eye which deserves a followup post. Copper inventories are rising rather dramatically.

Worldwide copper inventories and yearly change

As you can see from the chart above copper inventories are now at highs not seen since nearly 10 years ago. More importantly the year over year change is quite positive as well. The above graph is a month old but as we can see from a higher frequency chart total inventories may break 900 thousand tons soon.

Why inventories are rising so quickly could be due to several forces, some of the top of my head are:

Rising production -- New mines coming online.

Declining demand -- A sluggish Europe could be assisting in keeping demand down.

Hidden inventory being brought back onto the markets -- If this is a case of Dark Copper coming back into the official warehouses it would validate some theories regarding base metals being used as financing source in China. FT.com posts dated March 31, 2011 and April, 26 2012 provide good roundups of the possibility and mechanics.

Of course only hindsight knows why copper stocks are building right now. We have to wait to find out why.

The video I previously posted has incited a new round of Chinese Empty City Watching. Jim Chanos, the famous short seller, was recently on CNBC explaining his rationale and hinting at his short positions.

Last night 60 Minutes ran a piece on the housing bubble of China:

Link to video

I have written about the Chinese Housing Bubble at length and it is nice to see the popular media pick up on it as well. I wonder how much longer this can go on.

I recently stumbled across this video given at the Google campus regarding negotiating with the Chinese. While much has changed since this presentation in 2006 (Google is no longer in China and the consensus of inexorable healthy Chinese growth is now questioned) the perspectives on Chinese and American negotiating goals most likely have not.

I was a party to business negotiations in Taiwan in 2001 and personally experienced some of the negotiating tactics discussed in this video. Fortunately I had brushed up on some of this before the event and wasn't flustered by the time delaying or subtle put downs employed.

If any of my readers can confirm or deny any of the topics covered in this video I'd love to hear from you.

I had the pleasure of attending the 2012 Vail ValueX conference hosted by Vitaliy Katsenelson http://contrarianedge.com/valuex-vail/

While I will write more about my impressions here's a link to Jim Chanos' notes.

Getting accurate data regarding economic activity in the Middle Kingdom is always difficult. I've blogged about it before and have grown to look at circumstantial indicators for clues as to what's happening in there. Mr Chovanec and Soberlook are two blogs who've been writing about evidence of a slowdown for some time now.

One of those indicators is sliding back down again and is close to the panic lows of last fall. Iron Ore prices did not bounce much from the October lows and are now inching downward again.

News of the Chinese refusing to purchase previously ordered cargoes of Iron Ore and Coal is additional data supporting the slowdown thesis. A serious slowdown in China would not bode well for the world economy considering Europe's problems as well. Keep an eye on Iron prices. If they fall through the October floor I'd be cautious.

Mr. Hugh Hendry of Eclectica appears to have come out of his self imposed social hibernation. Below is a video from the Milken Institute conference where he is part of a panel discussing Europe's problems. It is a long video but I suggest you watch it.

While Mr. Hendry appears to be still very bearish about Europe I do agree with the person on his right that now is the time to start looking for opportunities. (note, I said LOOK) With all their problems and low stock prices there must be some incredible buys amongst all the wreckage that European austerity is creating. I'm not suggesting you buy now but start doing your homework. Anyone have any ideas? I'm open to suggestions.

Hugh Hendry (Hedge fund manager of Eclectica fund) recently released his April commentary which you will find below. (Thanks ValueWalk)

Mr. Hendry has been less visible recently so it is nice to hear his most recent thoughts. As always he provides some thought provoking ideas and historical analogs to our current situation. It will be very interesting to see if his ideas and predictions are correct. Like the name of his fund, his view are 'eclectic'.

Getting accurate information on China is a challenge. While its hard to prove they are making their numbers up I don't put much credence in many official statistics released from the Glorious Workers Paradise. (WSJ June 2011, Reuters December 2010)

Fortunately there are other ways of observing China, from their borders specifically. Trade statistics between the Middle Kingdom and the US is actually reported and available from US sources. The story they tell show of slowing trade between the countries in both directions.

Year over year % change of 3 month average

Source: Federal Reserve

While the graph above is smoothed and lagged quite a bit one can see both China and the US's decline in 2008/09 and China's massive resurgence in 2009 and the US a few months later.

Right now the story is also one of declining growth of trade in both directions.

Of course trade partners may and will shift their vendors around from country to country so this data should be looked at with some large error bars on the data, but this slowdown is something to keep an eye on as a coincident/lagging indicator of each countries economic trajectory.

The Baltic Dry Index (spot shipping rate for bulk commodities like iron ore, grain, coal, etc) recently fell off a cliff and has not seen these levels since the dark days of early 2009.

While one can say there are legitimate supply problems (a huge overhang of new ships coming online from the order surge pre financial crisis of 2009); to see such a dramatic drop is impressive and deserving of attention. I have been quite bearish on China for quite a while on this blog (although now that their market has been thrashed and policy changes appear to be taking place I may have to alter that opinion) and the sudden fall in the index may be due to a lack of import volume into China. We'll see in a little bit if this drop in the Baltic Dry foretells a real slowdown in China...

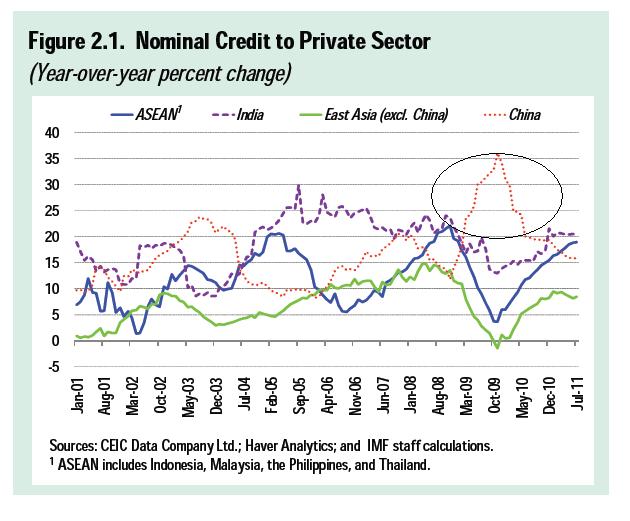

Earlier this month I highlighted the continued deceleration in Chinese lending growth from it's peak in late 2009. Just how massive their credit growth was unknown to me until this recent post and chart by Global Macro Monitor

The growth in lending right after the 2008/09 credit crisis is truly spectacular, even compared to other high growth Asian economies. I'll snicker even more when I hear talking heads gush about how the Chinese mandarins were able to 'navigate' their way through the economic crisis and their ability to manage such a large economy.

Bunk.

They just called up the bankers and said LEND.

The bankers asked, "How much?"

It was not some Chinese mastery of the economic cycle or superior technocratic skill; it was simply an ability to throw lots of money at the problem. Unfortunately for China the bill is now coming due.

It has been over a year since I last highlighted the slow decline in official lending statistics out of China. Since then not much has happened regarding the direction of Chinese lending growth; a slow decline continues.

I point you to Steve Keen's debtwatch for why the rate of growth in lending is important.

The rate of lending growth peaked in October 2009 and has been declining ever since. Compare this to the Chinese equity markets and you'll see how Chinese stocks haven't gone anywhere since October '09 either.

Unofficial lending is naturally harder to track but there are anecdotal signs of stress in this sector as well. http://historysquared.com/ and http://www.alsosprachanalyst.com/ are two good sites to follow the 'underground' lending market.

Some reading material for you from my twitter stream:

RT @edwardnh: Why the latest eurozone bail-out is destined to fail within weeks - Telegraph http://t.co/sgj8HQcn RT @credittrader: GReader: The Global Moral Hazard Dawns: Merkel Says "It Must Be Prevented That Others Come Seeking A Haircut" As... http://t.co/Tjd22kbQ RT @theanalyst_hk: $$ Jim Chanos: Not Impressed By The Europeans, And Still Shorting #Chinahttp://t.co/OvdXeWIr#economy#europe RT @JackHBarnes: Chart of the Day: North Dakota Annual Oil Production: http://t.co/lUWOqWst -- need to do more research myself on shale oil Transfer payments over time in US http://t.co/sxiw6sF8 RT @zerohedge: And Now, For Some Semblance Of Sanity, Here Is One Hour Of Hugh Hendry http://t.co/5A5Jwgxu -- separate post on this soon(tm) CITI: Failure To Trigger Greek CDS Could Cause The Whole Euro Bailout To Fall Apart http://t.co/TLDjUF7L -- be careful what you wish for Meanwhile in China a swan finally takes flight... http://t.co/Z8w40PKd -- Condo prices are falling hard. RT @AlephBlog: Fannie Squeezing Banks Makes 4% Mortgage a Mirage, Hinders Housing Rebound http://t.co/BKikceRX Higher lending standards fight lower rates RT @AlephBlog: Money managers and commodities, the case against http://t.co/ynsn1qT3 Graph shows $$ managers drove commodity prices http://t.co/eNKE3nFA RT @andrewyorks: *EU LEADERS CALL FOR BANKS TO HAVE 9% CORE CAPITAL LEVEL ok move that dial on the upper left to 9 http://t.co/WHLMk6Dm -- should be interesting when taking haircuts on Greek debt. Skyscraper taller than any in London or Tokyo opens in Chinese village of 2000. http://t.co/IvHoRw4j#thiswillnotendwell Underground bank lending in China - NPR - http://t.co/677IPKYK RT @historysquared: $$ The cash commodity trading firms that account for 1 trillion in annual revenue 50% of all transactions http://t.co/TqTvhHM1 RT @ftasia: Iron ore plummets to 15-month low: As Chinese steel mills cut production, the price of iron ore dropped 7.2 per ... http://t.co/RVfC48zy Blackberry outage made roads safer. http://t.co/agSNxNGX

A little more than six months ago I laid out a bearish case for the red metal, also known as Dr. Copper by those in the markets for its ability to predict future economic change. With the recent thrashing copper and many other risk assets have taken I thought revisiting the topic would be a good idea.

While China is a large factor in all base metals prices let's start with the Old World and the seemingly mundane issue of actually counting how much copper inventory is on hand. While this would appear to be as simple as looking up the LME (London Metal Exchange) and COMEX (US futures) inventory numbers it really isn't. The BBC ran a three part series on rising commodity prices in late May and spent nearly a third of the program on copper.

BBC Radio - Bubble Trouble - Part 1 - May 28,2011 BBC Radio - Bubble Trouble - Part 2 and 3 Ft.com blog highlighting the inventory issue

In part 2 around the seven minute mark the presenter takes a tour of a well known base metals warehouse in which the warehouse representative reveals only about 40% of the copper in the warehouse is registered as LME inventory. When I heard the words I had to replay it several times to ensure I understood that correctly; my brain almost rebelled at the concept of anyone just coming out and publicly stating such a figure. Now I'm not suggesting the LME reported amount is under counting European stocks by 40%, just that this one warehouse has a lot more copper inside its walls that is reported to LME. Please listen to at least part 2 of the radio series to get the full details. If it can happen in one warehouse in Rotterdam what is preventing it from happening elsewhere in the world?

So why is the copper 'hiding'? Some of it is because costs are cheaper to store it in a non registered warehouse versus an official LME warehouse. Another factor may be what is suspected to be going on in China. FT Alphaville has discussed import/export trading firms there are using copper as a credit funding vehicle because other more official forms of credit are drying up.

Here’s the gist of it.In the first instance, our source says, the strategy is not exclusive to copper markets but goes on across most commodity markets.

The banks call it “inventory financing”. And of course, we should stress, it is completely legal. The practice mainly involves pledging an asset in return for an exchange warrant or cash.

According to our source, traders can deposit copper in an exchange warehouse in order to receive a warrant which can then be used to gain financing, usually via a broker, and less a 15 or 20 per cent haircut needed to cover futures margin deposits (sometimes called margin or warrant financing).

Read the whole article to get the full weight of what they are doing. This copper-as-financing would help explain why copper continues to be imported even though for most of 2011 it has been cheaper on the domestic Shanghai exchange. For the credit focused copper trader the money created by the transaction has greater value than the actual copper, it is just a funding mechanism.

While the discount has been steadily falling one must understand China is a net importer of Copper; so why has it been cheaper to buy copper inside China?

Izabella Kaminska followed up a few weeks later with more details on the same copper-as-collateral trade

More worryingly however is that the primary use of copper in bonded warehouse appears to be as a financing mechanism to provide cheap working capital for various types of business often unrelated to the metallic industry.

Having just come back from China my impression is that more and more people are beginning to understand that a lot of copper that has been imported has not gone into furnaces, that it is held by both foreign and Chinese financial institutions and others and I do think that even at the top level in government there is now starting to be a concern of the impact of this speculation on China's economy. Because it is not just copper - it goes much deeper than that. With money which has been so freely available in recent years, and with negative deposit rates, any company or individual is very reluctant to hold funds on deposit. So they are looking for other means of investment and it goes into commodity markets generally - the stock market, it goes into manufacturing investment and so on so forth. Whether government does anything to stop this game going on I've no idea, but there is at least a realisation at a pretty senior level that these developments are ongoing.

Mr. Hunt also brings up the insidious problem of negative real interest rates in a growing economy. Empty cities such as Ordos are an example of what happens when people respond to the obvious distortion of losing money when you put it in a bank account.

The world No.1 copper producer, Chile's state-ownedCodelco, sounded a warning shot at the CESCO copper industrygathering in Santiago on Monday, saying copper stocks in China were abnormally high and needed to be watched carefully.

Figures are tossed about regarding how much inventory has been tied up in these financing deals but one never really knows how much until the real washout hits and people are forced to dump their positions.

That being said, some analysts are putting out huge numbers as to the extent of hidden inventory, again from ft.com blog

The ICSG data shows an increase in Chinese demand of 99% for the four years between 2005 and 2009 when Chinese GDP probably rose by about a third. Obviously, there cannot possibly have been such a massive rise in copper’s intensity of use in China. You can look through all the intensity of use curves for every commodity for every economy in history and you will never find a doubling in consumption against a one third increase in GDP over so short a period of time.

The numbers are large, around 4 million tonnes since the end of 2006. This dates from when global fabricators and others started to understand that a new paradigm in the copper market had begun. It was the involvement of the financial community by buying copper directly from producers and others and warehousing the metal outside the reporting system.

High inventories in bonded warehouses point to the possibility of destocking, which could hit copper prices on the London Metal Exchange (LME). As of this week, we estimate that total copper stocks in bonded warehouses in Shanghai (usually 80% of the national total) have hit 650 thousand tonnes (kt) – equivalent to roughly four weeks of China's domestic use, a record-high level (Chart 2). This is significantly higher than 550kt in late February and the 200kt average over the past three years.

ETFs have been a useful tool to allow banks to move risk off balance sheet. When a bank takes on risk through lending to or financing a big commodity player, say for an acquisition, there is a need to hedge potentially huge commodity exposure — so as sell to lock in the commodity price, and you couldn’t sell that volume easily into the terminal market; although you could transfer a large amount of exposure to investors through an ETF more easily. The only way this used to be done is by the bank taking proprietary risk, but they now have other risk issues and aren’t prepared to carry that sort of exposure.

Using ETFs becomes a mutuality of interest, with everyone moving to launch products to investors – retail and institutional – so that they can carry the risk instead. It’s all about de-risking your book. And you saw it in the dot com bust when investment banks pushed dotcoms, but offloaded the risk to investors. When the NASDAQ crashed the investors carried the bulk of the exposure.It all has similarities to the Abacus CDO. If you want to short the market you have to create the demand, like Paulson did. If you are an institutional advisor you can do that by hyping the commodity.

The actual import numbers going into China for both refined and scrap do not mesh well with the meme of voracious demand. On a year over year basis both are falling.

Furthermore the reported inventory numbers have been wandering around the 600k number for a while. Ironically the last time year over year inventory numbers dipped into negative territory for a while was 2008.

I'm not the only one who is not a copper bull. The Reformed Broker sums it nicely while debating a copper bull:

I will admit some of my thesis is based upon information that is not reported as cut and dried numbers that can easily be looked up on a computer screen but what I do find does not add up to the template of China hoovering up all known copper deposits in the universe:

Copper is cheaper in Shanghai than in London

Copper imports of all kinds are dropping

Public reports of a LOT of hidden copper stocks, in the Old Word as well as China and confirmed by Chileans

I could go on but you need to put in some work as well. Read over the links below. I saved a few bombshells for your discovery...