Last night 60 Minutes ran a piece on the housing bubble of China:

Link to video

I have written about the Chinese Housing Bubble at length and it is nice to see the popular media pick up on it as well. I wonder how much longer this can go on.

Monday, March 4, 2013

Thursday, February 21, 2013

A warning from the unemployment line

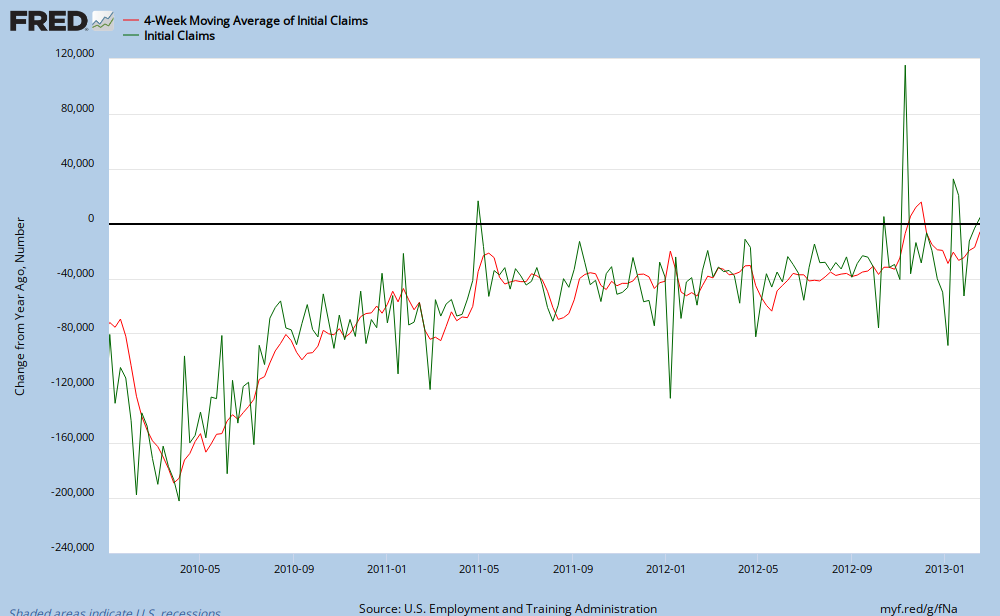

The weekly initial claims for unemployment data was released today and it is getting close to being a concern of mine.

As can be seen from this chart of *non seasonally adjusted and *4 week average of seasonally adjusted data, (the noisiest and smoothest interpretations of this data series) the rate of decline has effectively stopped. Yes there were some spikes upwards during the hurricane Sandy and blizzard Nemo, but the trend has started to move upwards after spending most of 2011 and 2012 fluctuating around an annual decline in jobs unemployment claims of ~40,000.

We are now near the break-even mark and if it starts to consistently go positive, (more people laid off now as compared to last year) this would be a very strong warning flag to the US economy.

Considering the recent payroll tax hike and other tax increases recently imposed it is possible we may see this happen.

|

| Year over year change, initial unemployed claims - Source Federal Reserve |

We are now near the break-even mark and if it starts to consistently go positive, (more people laid off now as compared to last year) this would be a very strong warning flag to the US economy.

Considering the recent payroll tax hike and other tax increases recently imposed it is possible we may see this happen.

Thursday, January 3, 2013

Employment, seasonality, and noise

The monthly employment report can be a high volatility day for the markets. The ADP report (BusinessInsider.com) came in above expectations and this was most likely the reason for early weakness in bond prices. (before the Fed Minutes release.) However how one looks at the data can change your perspective.

ADP data is shown in red, with Federal data shown in blue. Looking at the data, it does look quite random, great recession notwithstanding. It jerks up and down with no apparent order and the ADP data does not appear to track the Federal data well. No wonder the markets can be volatile on employment release days.

Let us look at the data a slightly different way ...

|

| Monthly employment numbers, ADP and Federal Source: Federal Reserve |

Let us look at the data a slightly different way ...

|

| Year over year change in employment, ADP and Federal Source: Federal Reserve |

Same data, just looking at a year over year percentage change instead of an absolute monthly change. Looks a little different doesn't it? There are minor variations in the two curves but not much. Looking at the data this way however, it appears we are on the downslope of employment growth and that great ADP number which was released today doesn't look so impressive does it?

I'm not implying what tomorrow's employment report will look like, just a hint that how you look at the data can make a big difference in what conclusions to draw.

Monday, December 31, 2012

The fiscal cliff of 1937

With all the current noise regarding the 'fiscal cliff' I thought a look back at when we had a real fiscal cliff would be interesting.

Steve Keen, an Australian economist I've mentioned before recently gave a presentation to members of Congress regarding the Fiscal Cliff of 1937.

Source: http://www.debtdeflation.com/blogs/2012/12/06/briefing-for-congress-on-the-fiscal-cliff-lessons-from-the-1930s/

In his presentation Mr. Keen describes the mechanism through which a dramatic tax increase coupled with an absolute cut in spending threw the US economy into a recession. From 1937 to '38 tax receipts when up ~25% and spending was cut ~8% While in the 1937 spending and taxes were a much smaller percentage of GDP, the large swings in their absolute numbers were enough to decrease the deficit from -2.5% to -0.1% or a change of 2.4% (source: White House)

Additionally the Federal Reserve shrank their balance sheet at the same time:

The combination of Fiscal and Monetary tightening pushed the economy back into recession. (Vertical gray lines on above graph.)

Right now we are experiencing a similar situation: The US economy is working off the excesses of a burst credit bubble and federal spending and deficits are at an all time high.

As you can see above, spending is at at a peacetime high and taxes are near a post WWII low. (Both relative to GDP.) Combine the two and you have the largest peacetime deficit from 1900 onward. (The data from the White House doesn't go back any further than 1900, so there may be another time period before then however I doubt we have experienced peacetime 10+% budget deficits before.)

A ~2.5% GDP growth rate after coming out of a recession is quite low as compared to historical norms.

Steve Keen, an Australian economist I've mentioned before recently gave a presentation to members of Congress regarding the Fiscal Cliff of 1937.

In his presentation Mr. Keen describes the mechanism through which a dramatic tax increase coupled with an absolute cut in spending threw the US economy into a recession. From 1937 to '38 tax receipts when up ~25% and spending was cut ~8% While in the 1937 spending and taxes were a much smaller percentage of GDP, the large swings in their absolute numbers were enough to decrease the deficit from -2.5% to -0.1% or a change of 2.4% (source: White House)

Additionally the Federal Reserve shrank their balance sheet at the same time:

|

| The wrong time to anti-QE Source: Federal Reserve |

The combination of Fiscal and Monetary tightening pushed the economy back into recession. (Vertical gray lines on above graph.)

Right now we are experiencing a similar situation: The US economy is working off the excesses of a burst credit bubble and federal spending and deficits are at an all time high.

|

| Spending and Taxes from 1930 on Source: White House |

Today we can see the credit bubble bursting in a chronically high unemployment rate and sluggish GDP growth. Unlike other downturns, our GDP did not rebound much.

|

| Real US GDP Source: Federal Reserve |

A ~2.5% GDP growth rate after coming out of a recession is quite low as compared to historical norms.

Raising taxes too quickly combined with actual spending cuts on an already slowly growing economy could send us immediately into a recession. This is what has Wall Street in a current tizzy and is already hitting consumer confidence.

Predictions about the future are tricky, especially when politicians are involved.

How much taxes go up, and if there are any actual spending cuts will determine how much of a fiscal drag hits the economy in 2013. Right now it's all speculation and I'm not going to try to predict what Congress and the President will eventually agree to, before or after January 1, but there are a few items which appear certain:

How much taxes will go up and on whom is the unknown and that is what is creating uncertainty in the mind of corporations and individuals. Until we have clarity both the markets and consumer actions may be volatile.

Additional reading:

http://www.ritholtz.com/blog/2012/12/what-is-the-fiscal-cliff/

http://www.cringely.com/2012/12/16/dr-al-explains-the-so-called-so-called-fiscal-cliff/

http://soberlook.com/2012/11/putting-fiscal-cliff-in-perspective.html

I actually wrote about this 2+ years ago as I was studying the history of the Great Depression.

http://merrillovermatter.blogspot.com/2010/06/is-steep-yield-curve-leading-us-astray.html

Thanks to

@mbusigin 1937 fed data

@AlephBlog When is a 'cut' really a 'cut' in Washington speak (hint, not very often)

Predictions about the future are tricky, especially when politicians are involved.

How much taxes go up, and if there are any actual spending cuts will determine how much of a fiscal drag hits the economy in 2013. Right now it's all speculation and I'm not going to try to predict what Congress and the President will eventually agree to, before or after January 1, but there are a few items which appear certain:

- Taxes will go up, but not as much as 1937 on a percentage basis

- Spending will most likely not decline on an absolute basis

- Federal spending is a much larger percentage of the economy than in 1937

- The Federal Reserve will NOT shrink its balance sheet in 2013

How much taxes will go up and on whom is the unknown and that is what is creating uncertainty in the mind of corporations and individuals. Until we have clarity both the markets and consumer actions may be volatile.

Additional reading:

http://www.ritholtz.com/blog/2012/12/what-is-the-fiscal-cliff/

http://www.cringely.com/2012/12/16/dr-al-explains-the-so-called-so-called-fiscal-cliff/

http://soberlook.com/2012/11/putting-fiscal-cliff-in-perspective.html

I actually wrote about this 2+ years ago as I was studying the history of the Great Depression.

http://merrillovermatter.blogspot.com/2010/06/is-steep-yield-curve-leading-us-astray.html

Thanks to

@mbusigin 1937 fed data

@AlephBlog When is a 'cut' really a 'cut' in Washington speak (hint, not very often)

Thursday, November 15, 2012

Social media and... war

Last night I saw something rather peculiar come up on my twitter stream, retweeted by someone I follow:

Errr. What is this? Turns out both the Israeli Defense Forces ( @IDFSpokesperson ) and Hamas ( @AlqassamBrigade ) are live tweeting the current conflict between them in Gaza!

Please note: This post is not about which side is the aggrieved party or who is at fault regarding this situation, merely the fact that both parties are using Twitter, Twitter pics, blogs, and YouTube to present their side of the story in an attempt to sway public opinion to their side. I'm not going to show either sides photos, videos or blog posts as the information can be quite graphic. Click on either parties twitter stream if you are interested in the gory details.

What I find morbidly fascinating is the idea of a military conflict being live tweeted. It certainly is a Brave New World we live in.

Errr. What is this? Turns out both the Israeli Defense Forces ( @IDFSpokesperson ) and Hamas ( @AlqassamBrigade ) are live tweeting the current conflict between them in Gaza!

Please note: This post is not about which side is the aggrieved party or who is at fault regarding this situation, merely the fact that both parties are using Twitter, Twitter pics, blogs, and YouTube to present their side of the story in an attempt to sway public opinion to their side. I'm not going to show either sides photos, videos or blog posts as the information can be quite graphic. Click on either parties twitter stream if you are interested in the gory details.

What I find morbidly fascinating is the idea of a military conflict being live tweeted. It certainly is a Brave New World we live in.

Tuesday, November 13, 2012

Hugh Hendry watch, belatedly -- Buttonwood conference

Here's the latest from Hugh Hendry at the Buttonwood conference a few weeks back. Sorry for the delay in posting this and frequency of posts in general; I've been very busy in the personal and business realm.

Watch live streaming video from theeconomist at livestream.com

ht: PragCapFriday, October 12, 2012

Inflation expectations and QE(infinity)

I have posted before regarding inflation expectations in the US treasury market and I need to give you an update, especially so considering the recent round of QE as announced by the Federal Reserve.

A refreshed chart from the Fed of the inflation expectation spread (10 year nominal yield minus 10 year TIPS yield) teases out some interesting items to consider.

Note how we have recently broke above the 2.5% Since the GFC it has rarely breached this mark and did not stay there for long.

Now look at when previous QE's were initiated. A graph by dshort.com does the job.

A refreshed chart from the Fed of the inflation expectation spread (10 year nominal yield minus 10 year TIPS yield) teases out some interesting items to consider.

|

| 10 year nominal Treasuries minus 10 year TIPS (source: Federal Reserve) |

Note how we have recently broke above the 2.5% Since the GFC it has rarely breached this mark and did not stay there for long.

Now look at when previous QE's were initiated. A graph by dshort.com does the job.

While they are not to the same scale, you will notice the first round of QE was initiated during the deep dark days of the financial crisis. The inflation expectation spread was near its low of the series and the world looked bleak.

QE2 was discussed mid 2010 and also coincided with an interim dip in the inflation spread at around 1.5%

QE(infinity) was just announced and our inflation expectation spread is already near the highs of the entire series.

While the Fed and other market participants have their own flavor of inflation expectations they look at this series is near its highs. Before the GFC this spread didn't venture much higher and the Fed thinks they can get it higher now? The future is subject to change (of course) but unless we get some serious wage growth it appears to me the Fed is pushing up against a long term inflation expectation wall.

As an example here's nominal Personal Consumption Expenditures. It has been on a secular decline since the inflation days of the 80's and also notice how it recently peaked and appears to be rolling over again (ahem)

|

| Nominal PCE - Source Federal Reserve |

For some additional context here's the 10 year nominal and TIPS yield since 2004. Notice how now 10 year TIPS are now going for a negative real yield.

Disclosure: Considering selling/shortening duration on some TIPS positions

Subscribe to:

Posts (Atom)