Hedge fund manager Hugh Hendry has a long conversation on BBC Hardtalk regarding taking risk and the public bailouts. It is refreshing to see a 25+ minute discussion regarding taking risk and losses, unlike the nanosecond blipverts so common in American business TV.

Part 1

Part 2

Part 3

Wednesday, September 22, 2010

Tuesday, September 21, 2010

Shadow inventory: More homes coming

I have spoken before about how the supply of forced sale (foreclosed or short sale) inventory continues to increase but may be close to peaking. Here's an article stating the peak is not yet in and we have more to come:

From Realestatechannel comes some rather scary data regarding how the pipeline continues to be filled and they see no let up on new supply being dumped on the market.

ht: PragCap

From Realestatechannel comes some rather scary data regarding how the pipeline continues to be filled and they see no let up on new supply being dumped on the market.

If this were early 2005, one could claim that 40% of homeowners who were delinquent 90 days or longer would eventually bring the mortgage current. But the cure rate has plunged along with home prices. As early as one year ago, the cure rate had dropped to almost zero. A delinquency of 90+ days now means almost certain foreclosure or short sale.

. . . To come up with a total for the shadow inventory, let's first add the total number of loans in default to those delinquent 90 days or more since we know that these loans are headed for foreclosure or a short sale. That comes to 4.5 million properties. Based on the cure rate for loans delinquent at least 60 days, we will add 95% of those 60-day delinquencies. That is an additional 723,000 residences. For the same reason, we will add 70% of those delinquent for at least 30 days - 1.25 million properties.

And, of course, let's not forget the REOs that have not yet been placed on MLS listings by the bank servicers. We'll be conservative and estimate them at 500,000. Adding all of these together, we come up with a total of roughly 6.97 million residences which are almost certainly going to be thrown onto the resale market as distressed properties at some point in the not-too-distant future. This massive number of homes will put enormous downward pressure on sale prices. To believe that prices are firming now is to completely ignore this shadow inventory. Ignore it at your own risk.I suggest you read the whole article.

ht: PragCap

Monday, September 20, 2010

One small facet of the the mortgage mess

NPR (National Public Radio) has a great ongoing series about the mortgage mess. As a centerpiece to the series they purchased a slice of one very sick package of mortgages and are investigating the mortgages inside it. So far they have found some serious mortgage fraud as well as some other interesting stories. Take a look at one small facet of the housing bubble:

NPR: Planet Money's Toxic Asset

ht: NicTrades

NPR: Planet Money's Toxic Asset

ht: NicTrades

Thursday, September 16, 2010

The Humans are dead -- At least to the HFT computers

For those of you who aren't knee deep in the markets, you may not know about the HFT (high frequency trading by computers) and their affects on the markets. HFT was implicated in the May 'flash crash' and with the declining volume in the stock market it appears most trading is between computers. In that spirit I present a more humorous slant on the entire situation:

Here's the acoustic version:

http://www.youtube.com/watch?v=WGoi1MSGu64

And some news regading HFT systems getting fined (Zero Hedge)

Update: The Reformed broker has some new HFT toys for Christmas! :)

Here's the acoustic version:

http://www.youtube.com/watch?v=WGoi1MSGu64

And some news regading HFT systems getting fined (Zero Hedge)

Update: The Reformed broker has some new HFT toys for Christmas! :)

Tuesday, September 7, 2010

Oil inventories creeping upwards

Looking at total US oil and petroleum products inventory levels you will see they are at 20 year peaks! The OECD is also above its 5 year average inventory levels.

* Emerging market demand and specifically China is a great unknown.

* The Iran / Israel situation is keeping people jumpy.

* The financialization of commodities also provides a firm bid on oil prices.

* Hurricane season is just warming up in the US. We'll see how much carnage they produce.

Here's some previous entries on the topic of hurricane season:

http://merrillovermatter.blogspot.com/2009/08/weather-and-oil.html

http://merrillovermatter.blogspot.com/2009/09/so-far-no-hurricanes-this-year.html

Monday, August 30, 2010

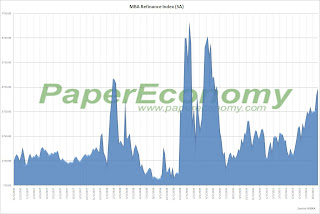

The Fed is exacerbating the move in bonds

The recent Federal Reserve August 10 announcement to reinvest principal paydowns from its very large (1+ Trillion) mortgage backed security portfolio into longer dated US Treasury securities is providing additional downward pressure on home loan rates.

Because interest rates have dropped since the completion of purchases, (March 31,2010: Federal Reserve MBS Faq) the frequency of individual homeowners refinancing has gone up. As such cash flows back to the Federal Reserve have increase to a rate higher than initially expected.

Because interest rates have dropped since the completion of purchases, (March 31,2010: Federal Reserve MBS Faq) the frequency of individual homeowners refinancing has gone up. As such cash flows back to the Federal Reserve have increase to a rate higher than initially expected.

If you look at the first chart attached you can see 10 year bond prices were already marching higher before the Federal Reserve reinvestment announcement of August 10. (Shown here as a white vertical line) Since then they have continued higher.

These principal payments are being invested in longer term Treasury Bonds which then pressures long term interest rates down, causing more refinancings, causing more cash to be sent to the Fed which then buys more Treasury bonds. Do you see the pattern here? This does not mean long bond yields WILL drop, but it places additional pressure for them to go down until the current refinancing burst (Paper Economy) ends.

These principal payments are being invested in longer term Treasury Bonds which then pressures long term interest rates down, causing more refinancings, causing more cash to be sent to the Fed which then buys more Treasury bonds. Do you see the pattern here? This does not mean long bond yields WILL drop, but it places additional pressure for them to go down until the current refinancing burst (Paper Economy) ends.

I wonder if the Fed thought this all through?

If you look at the first chart attached you can see 10 year bond prices were already marching higher before the Federal Reserve reinvestment announcement of August 10. (Shown here as a white vertical line) Since then they have continued higher.

I wonder if the Fed thought this all through?

Wednesday, August 25, 2010

Refinance your home if you haven't done so already

The Wall Street Journal had a recent article about shopping for a home loan:

The interest rates for 30-year fixed-rate mortgages are in free fall, averaging just 4.44% on Aug. 12, according to Freddie Mac. Not only was that down from 5.07% in January, it was the lowest since Freddie began keeping records in 1970.As the article mentioned some very good deals can be found at smaller banks and credit unions. Our family's primary checking account is at a credit union and their excellent customer service and low fees are a stark contrast to the national chains.

But even better deals can be found at smaller banks and credit unions.

"I've found that my clients can get routinely better rates by heading to a more regional lender and forgoing the bigger lenders," says Sean Satkus, a real-estate agent in the Washington, D.C., area.

The differences can be stark. On average, the three biggest banks—Bank of America Corp., Wells Fargo & Co. and J.P. Morgan Chase & Co.—offer rates of 4.66% on 30-year fixed mortgages for home purchases, according to Bankrate.com. By contrast, St. Louis's Heartland Bank is offering a rate of 4.50%. Acacia Federal Savings Bank comes in at 4.25%. And Rockland Trust Co. in Boston is offering just 4.13%. (None of these offers include "points," or extra fees to secure lower rates.).

If you are in the position to refinance and have questions give me a ring and we can talk about some of the options / pitfalls when looking for a new mortgage.

Subscribe to:

Posts (Atom)